Innovative risk management solutions for the modern employer health plan.

Innovative risk management solutions for

the modern employer health plan.

FEATURED IN:

ABOUT THE FIRM ________

- MEN OF INNOVATION 2025 -

- LEADERS IN FINANCE 2026 -

FEATURED IN:

________

ABOUT THE FIRM

Fortune 100

solutions.

Middle-market execution.

HPX Partners is a boutique insurance services firm helping midsized organizations overcome cost and quality challenges in their employee health benefits through specialized solutions in alternative health plan funding.

Fortune 100 Solutions.

Middle-market execution.

HPX Founder & CEO, Matt Luciani

A modern approach to employer healthcare.

HPX works with organizations that currently administer health benefits through conventional carrier-bundled insurance models and struggle with rising premiums, limited transparency, and declining member satisfaction resulting from the structural limitations of those arrangements.

Drawing from risk management solutions historically utilized by Fortune 100 enterprises, HPX reframes health plan administration from an insurance-buying exercise into a data-driven healthcare purchasing strategy.

Rather than relying on a single carrier to finance, administer, and coordinate healthcare services, HPX helps employers evaluate each function independently and align specialized partners across the areas of provider contracting, pharmacy benefit management, third-party administration, and risk financing to deliver superior value, transparency, and performance.

Combining institutional expertise with first-rate execution, HPX helps plan sponsors gain greater control over healthcare spending, improve access and affordability for plan members, and drive employee engagement into the future.

INDUSTRY OUTLOOK ________

________

INDUSTRY OUTLOOK

Limitations of carrier-bundled healthcare.

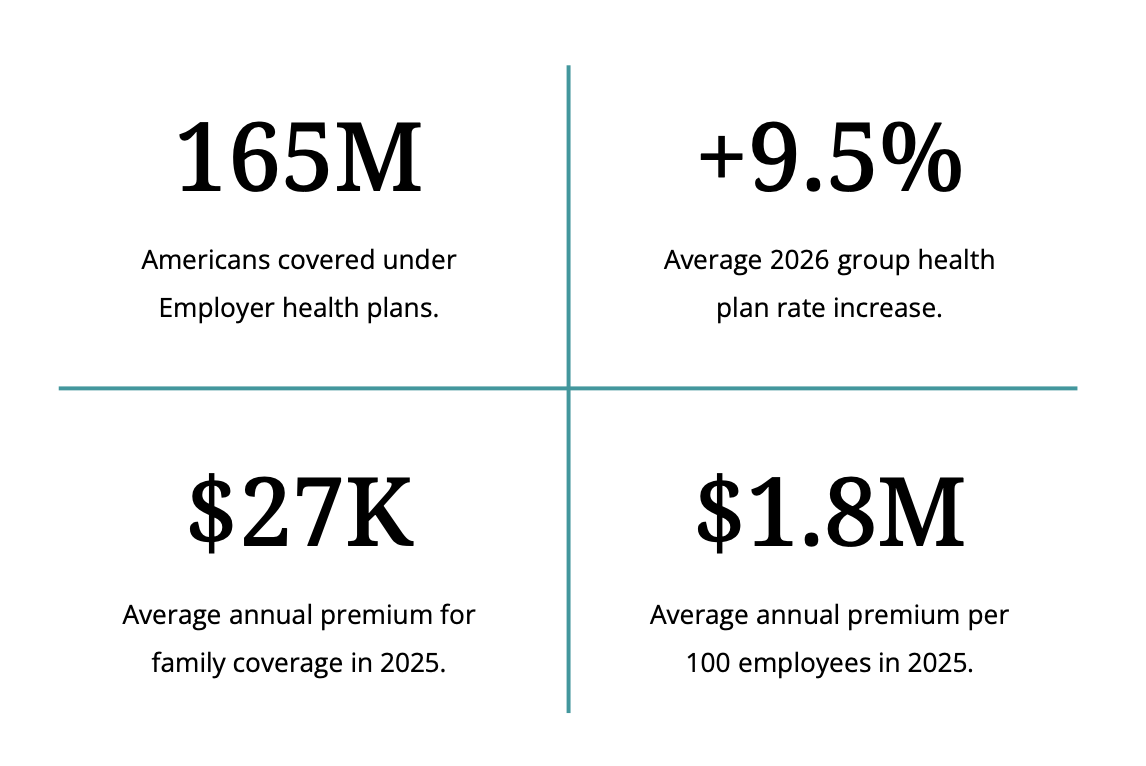

Employer health plan costs have risen steadily over the last decade, driven largely by inflation in medical and pharmacy care. Midsize employers remain particularly vulnerable to these pressures because most continue to purchase healthcare through conventional carrier-bundled insurance structures that centralize provider pricing, pharmacy administration, and member navigation within a single insurance platform.

While these models historically offered administrative simplicity, they were designed for standardized mass administration rather than pricing efficiency, transparency, or modern patient expectations. As healthcare costs continue to accelerate, many employers are finding that conventional insurance arrangements provide limited flexibility to meaningfully influence the underlying drivers of plan performance.

Expansion of strategic healthcare purchasing.

Expansion of strategic healthcare purchasing

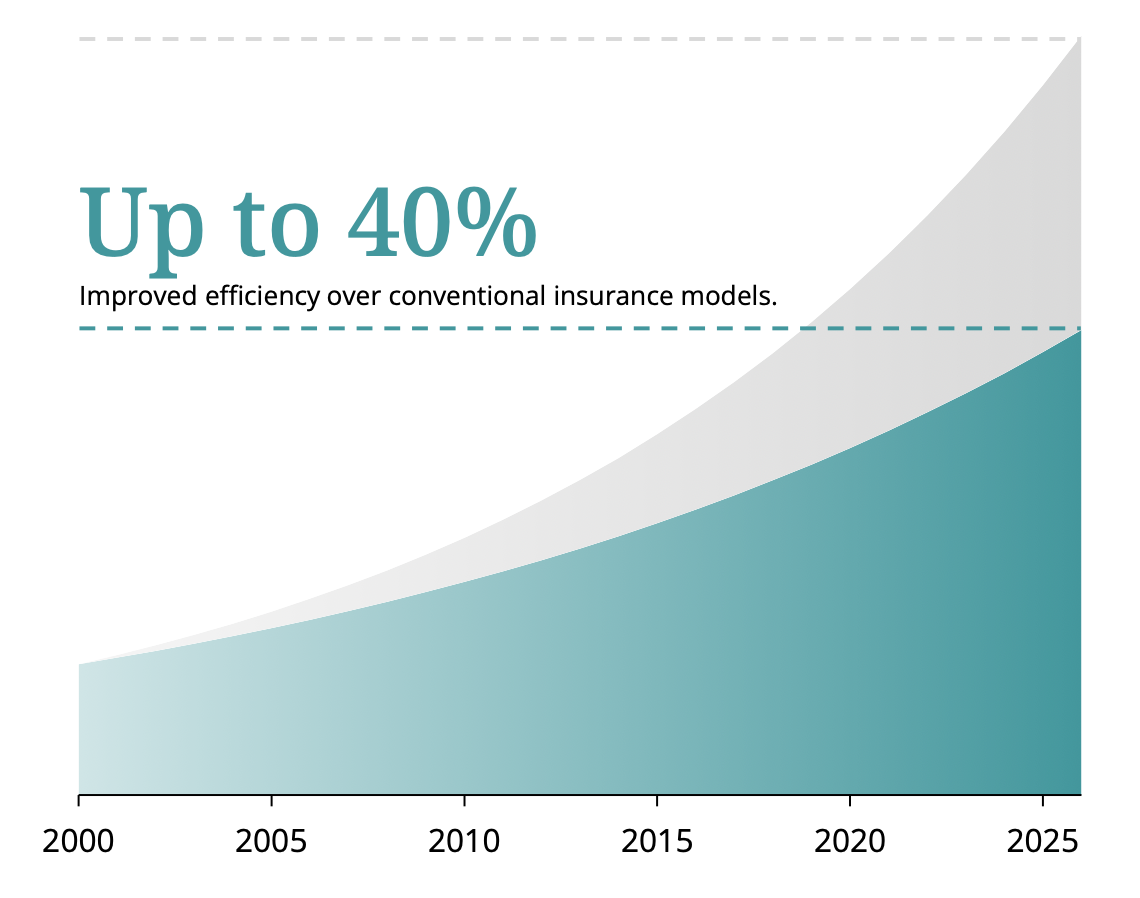

Large enterprise employers have increasingly separated healthcare delivery functions from traditional insurance arrangements, leveraging specialized administrators to improve pricing, transparency, and patient experience. Once reserved primarily for Fortune 100 organizations, these strategies are becoming increasingly accessible to midsize employers with as few as 100 plan members.

Looking ahead, the long-term sustainability of midsize employer health plans will depend less on annual insurance negotiations and more on the ability to strategically manage healthcare purchasing itself. Employers that modernize their plan infrastructure and source healthcare through more efficient contracting models will be better positioned to control costs, improve workforce satisfaction, and maintain competitive benefits offerings in an increasingly complex healthcare environment.

Setting new course

to 2030 and beyond.

OUR APPROACH ________

________

OUR APPROACH

Healthcare delivery before insurance mechanism.

Most midsize employers continue to manage health benefits through an insurance procurement mindset, focusing primarily on the selection of a fully insured, level funded, or self-insured funding structure.

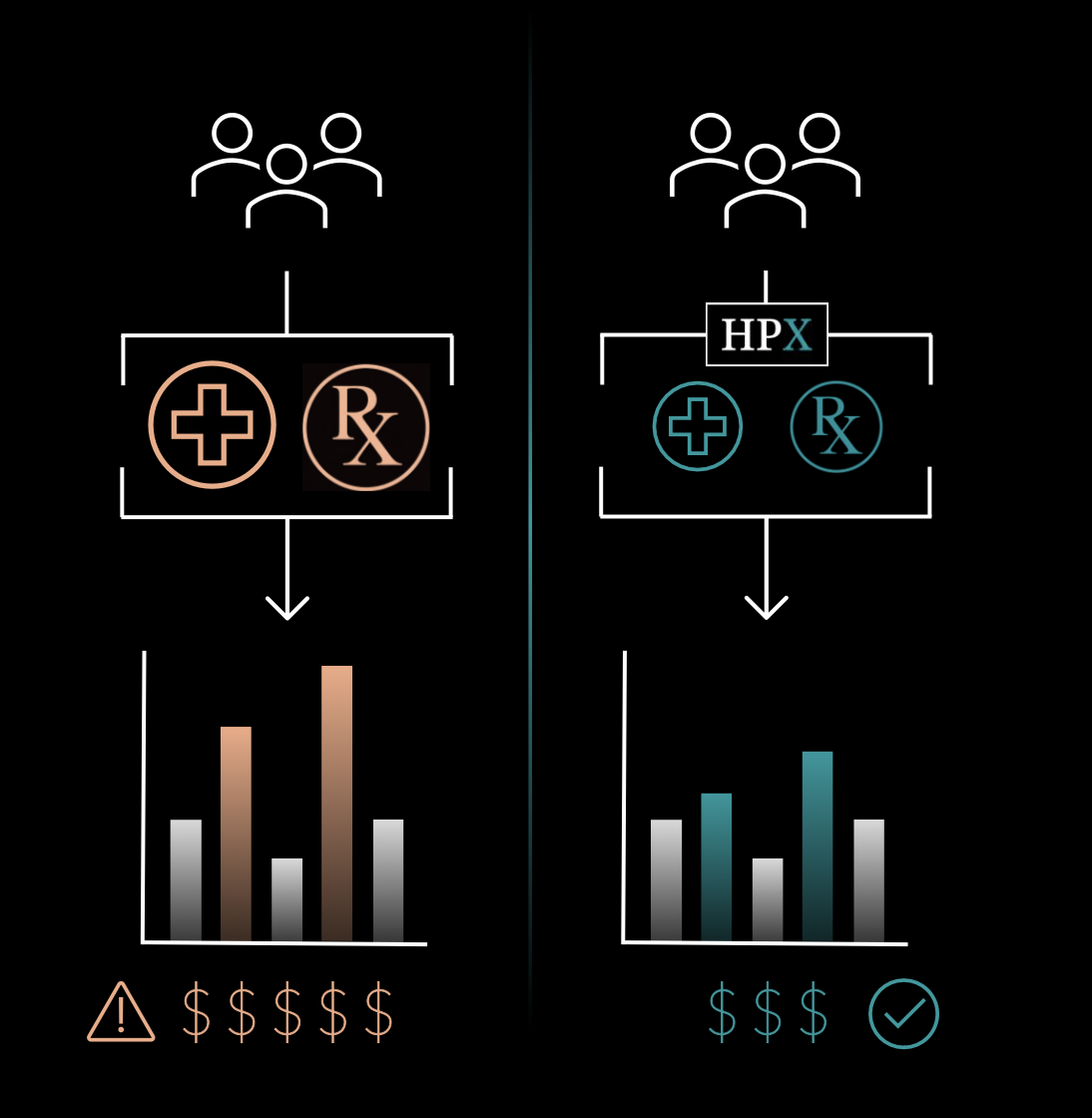

HPX operates from a different premise: employer health plans are not simply insurance products, but complex healthcare purchasing systems that determine how medical and pharmacy services are priced, sourced, administered, and accessed across the workforce.

Through this lens, we help employers separate healthcare purchasing functions from the risk financing arrangement, allowing them to proactively manage the underlying drivers of cost, quality, and member experience rather than simply reacting to annual insurance renewals.

Rather than centering strategy around the insurance carrier itself, HPX focuses on restructuring the core operating framework of the health plan through specialized administrative partnerships across three key areas:

- Provider Network Contracting

- Pharmacy Benefit Management

- Third Party Administration

By optimizing these healthcare purchasing functions independently from the insurance layer, employers gain greater control over provider pricing, pharmacy economics, patient navigation, and overall plan performance.

Once the healthcare delivery framework has been properly engineered, HPX structures the appropriate Risk Financing strategy to support the model, creating a more efficient, transparent, and sustainable health plan over the long term.

Engineered for high performance.

Don’t compare quotes.

Solve for pricing efficiency.

OUR PROCESS ________

________

OUR PROCESS

Don’t compare quotes.

Solve for X.

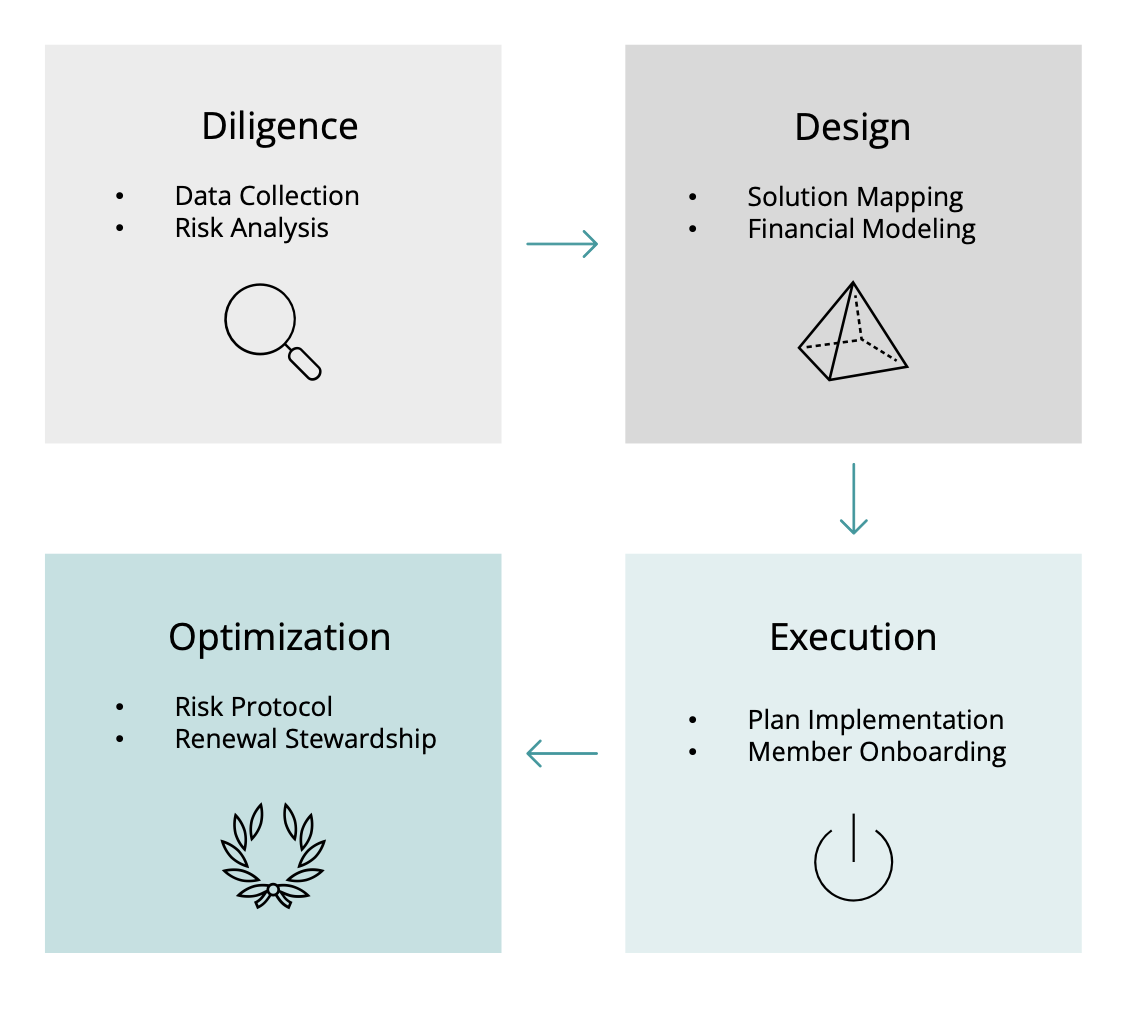

HPX guides clients through four phases of health plan transformation, beginning with Diligence and Design to evaluate existing plan structures, identify inefficiencies, and develop a strategic blueprint for modernization.

From there, we transition into Execution and Optimization, coordinating implementation, vendor alignment, ongoing analytics, and active risk management oversight across the healthcare purchasing system.

The HPX process transforms health plan management from a reactive annual renewal exercise into a disciplined long-term operating strategy designed to improve plan economics, modernize the patient experience, and create sustainable performance over time.

Experience the HPX difference.

Other Firms

Brokers selling insurance products.

"We quote the entire market."

Generalists juggling multiple disciplines.

Benefits, commercial insurance, retirement, personal lines, etc.

Year-to-year and renewal-reactive.

Wait for renewal results and spreadsheet alternatives.

Preservation of legacy revenues.

Rigid, slow to adapt, and serving shareholder interests.

HPX Partners

Innovative risk management solutions.

"Don't compare quotes. Solve for X."

Specialists delivering exceptional results.

Fortune 100 strategies, adapted for midsize employers.

Multi-year vision with proactive approach.

Year-round risk management, softening renewal impact.

Founder-led innovation.

High-touch, quick to adapt, and driving change in the market.

Plan Profile: 140 employees; $2.1M plan fund.

Problem: Rising prescription drug costs.

Solution: Independent pharmacy benefit manager.

Outcome: $350K annual plan savings.

Read Case Study →

Plan Profile: 100 employees; $1.3M plan fund.

Problem: Forfeiture of claims surplus to carrier.

Solution: Strategic risk financing arrangement.

Outcome: $120K annual plan savings.

Read Case Study →

Plan Profile: 210 employees; $3.5M plan fund.

Problem: Excess chemotherapy reimbursement.

Solution: High-performance third-party administration.

Outcome: $400K annual plan savings.

Read Case Study →

Plan Profile: 180 employees; $2.6M plan fund.

Problem: Network and coverage restrictions.

Solution: Independent third-party administration.

Outcome: Unrestricted patient healthcare navigation.

Read Case Study →

Plan Profile: 150 employees; $2.5M plan fund.

Problem: Rising provider and facility reimbursements.

Solution: High-performance medical network contract.

Outcome: $180K annual plan savings.

Read Case Study →

Plan Profile: 570 employees; $13M plan fund.

Problem: Inefficient and opaque claim funding.

Solution: Efficient and transparent risk financing.

Outcome: $1.4M annual plan savings.

Read Case Study →

Plan Profile: 160 employees; $2.1M plan fund.

Problem: Prescription drug rebate waste.

Solution: Independent pharmacy benefit manager.

Outcome: $250K annual plan savings.

Read Case Study →

Plan Profile: 70 employees; $1M plan fund.

Problem: Insufficient population risk scale.

Solution: Group-purchased risk financing.

Outcome: $120K annual plan savings.

Read Case Study →

Plan Profile: 140 employees; $2.1M plan fund.

Problem: Rising prescription drug costs.

Solution: Independent pharmacy benefit manager.

Outcome: $350K annual plan savings.

Read Case Study →

Plan Profile: 100 employees; $1.3M plan fund.

Problem: Forfeiture of claims surplus to carrier.

Solution: Strategic risk financing arrangement.

Outcome: $120K annual plan savings.

Read Case Study →CASE STUDIES ________

________

CASE STUDIES

Plan Profile: 140 employees; $2.1M plan fund.

Problem: Rising prescription drug costs.

Solution: Independent pharmacy benefit manager.

Outcome: $350K annual plan savings.

Plan Profile: 210 employees; $3.5M plan fund.

Problem: Excess chemotherapy reimbursement.

Solution: High-performance third-party administration.

Outcome: $400K annual plan savings.

Plan Profile: 180 employees; $2.6M plan fund.

Problem: Network and coverage restrictions.

Solution: Independent third-party administration.

Outcome: Unrestricted patient healthcare navigation.

Plan Profile: 150 employees; $2.5M plan fund.

Problem: Rising provider and facility reimbursements.

Solution: High-performance medical network contract.

Outcome: $180K annual plan savings.

Plan Profile: 570 employees; $13M plan fund.

Problem: Inefficient and opaque claim funding.

Solution: Efficient and transparent risk financing.

Outcome: $1.4M annual plan savings.

Plan Profile: 160 employees; $2.1M plan fund.

Problem: Prescription drug rebate waste.

Solution: Independent pharmacy benefit manager.

Outcome: $250K annual plan savings.

Plan Profile: 70 employees; $1M plan fund.

Problem: Insufficient population risk scale.

Solution: Group-purchased risk financing.

Outcome: $120K annual plan savings.

Plan Profile: 100 employees; $1.3M plan fund.

Problem: Forfeiture of claims surplus to carrier.

Solution: Strategic risk financing arrangement.

Outcome: $120K annual plan savings.